Author:

Christy White

Date Of Creation:

10 May 2021

Update Date:

1 July 2024

Content

- To step

- Part 1 of 6: Understanding bitcoins

- Part 2 of 6: Getting to know the pros and cons of using bitcoins

- Part 3 of 6: Set up storage for bitcoins

- Part 4 of 6: Exchanging Bitcoins

- Part 5 of 6: Using a salesperson

- Part 6 of 6: Using Bitcoin ATMs

- Tips

Bitcoin is an online alternative currency system that acts as a form of digital money. Bitcoin is used both as an investment and as a means of payment for goods and services and is touted as a way to do so without third parties. Despite its increasing popularity, bitcoin is still accepted by few companies. Investing in bitcoin can be risky. It is very important to understand what bitcoin is and what the pros and cons are before purchasing bitcoin.

To step

Part 1 of 6: Understanding bitcoins

Understand the basics of bitcoin. Bitcoin is a completely virtual currency that allows consumers to exchange money for free without a third party (such as a bank, credit card company or other financial institution). Bitcoin is not regulated or controlled by a central authority such as De Nederlandse Bank and all bitcoin transactions take place in an online market, where the users are anonymous and almost untraceable.

Understand the basics of bitcoin. Bitcoin is a completely virtual currency that allows consumers to exchange money for free without a third party (such as a bank, credit card company or other financial institution). Bitcoin is not regulated or controlled by a central authority such as De Nederlandse Bank and all bitcoin transactions take place in an online market, where the users are anonymous and almost untraceable. - Bitcoin allows you to exchange money instantly with anyone anywhere in the world without having to open a business account or use a bank or financial institution.

- No names are required to transfer money, so there is little risk of identity fraud.

Learn about it Bitcoin mining. To understand bitcoin itself, it is important to understand Bitcoin mining, which is the process by which Bitcoin is created. although mining complicated, the basic idea behind it is that every time two people enter into a Bitcoin transaction, this transaction is digitally recorded by computers in a transaction log that describes all the details of the transaction (such as the time and who owns how many bitcoins).

Learn about it Bitcoin mining. To understand bitcoin itself, it is important to understand Bitcoin mining, which is the process by which Bitcoin is created. although mining complicated, the basic idea behind it is that every time two people enter into a Bitcoin transaction, this transaction is digitally recorded by computers in a transaction log that describes all the details of the transaction (such as the time and who owns how many bitcoins). - These transactions are then shared publicly into something a block chain and which lists all transactions and who owns how much bitcoin.

- Bitcoin miners are people with computers who constantly monitor the block chain to make sure it is up to date. They are the ones who confirm the transactions and in return they get a payment in bitcoin, which increases the total stock.

- Because bitcoin is not overseen by a central authority, mining ensures that the person transferring the bitcoin gets enough, that the agreed amount is transferred, and that the balance of each participant in the transaction is correct afterwards.

Learn about the legal aspects of bitcoin. Recently, new guidelines for virtual currencies were announced to combat money laundering. These new guidelines will regulate bitcoin exchanges, but leave the rest of the bitcoin economy alone for the moment.

Learn about the legal aspects of bitcoin. Recently, new guidelines for virtual currencies were announced to combat money laundering. These new guidelines will regulate bitcoin exchanges, but leave the rest of the bitcoin economy alone for the moment. - The bitcoin network is resistant to government interference and has built a loyal following among those involved in illegal activities such as drug trafficking and gambling due to its anonymous exchange of money.

- Ultimately, governments could conclude that Bitcoin is a money laundering tool and look for ways to stop it. It would be a daunting task to shut down Bitcoin completely, but intensive government regulation could put the system underground. This could limit the value of bitcoins as a legitimate means of payment.

Part 2 of 6: Getting to know the pros and cons of using bitcoins

Be aware of the benefits of bitcoin. The main benefits of bitcoins are low fees, identity fraud protection, payment fraud protection and instant money transfer.

Be aware of the benefits of bitcoin. The main benefits of bitcoins are low fees, identity fraud protection, payment fraud protection and instant money transfer. - Low costs. Unlike traditional financial systems, where the system itself (such as PayPal or a bank) is compensated with a fee, Bitcoin skips this entire system. The Bitcoin network is maintained by the miners, who are compensated with new Bitcoin.

- Protection against identity fraud. No name or other personal information is required for Bitcoin use, just an ID for your digital one wallet (the vehicle you use to send and receive Bitcoin). Unlike a credit card, where the counterparty has full insight into your ID and credit options, Bitcoin users trade completely anonymously.

- Payment Fraud Protection. Since bitcoins are digital, they cannot be counterfeited, which provides protection against payment fraud. In addition, transactions cannot be reversed, such as with a credit card refund.

- Instant transfer and settlement. Normally, when transferring money, there are significant delays, holdings, or other obstacles. The lack of a third party means that money can be transferred between two people instantly and with ease, without the complexities, delays and costs associated with purchases between parties using different currencies and providers.

Be aware of the drawbacks of using Bitcoin. In a traditional bank transaction, if someone trades fraudulently with your credit card or if the bank goes bankrupt, there are laws in place to limit the harm to consumers. Bitcoin, unlike traditional banks, does not have a safety net in case your Bitcoins are lost or stolen. There is no intermediary power to compensate you for lost or stolen bitcoins.

Be aware of the drawbacks of using Bitcoin. In a traditional bank transaction, if someone trades fraudulently with your credit card or if the bank goes bankrupt, there are laws in place to limit the harm to consumers. Bitcoin, unlike traditional banks, does not have a safety net in case your Bitcoins are lost or stolen. There is no intermediary power to compensate you for lost or stolen bitcoins. - Keep in mind that the bitcoin network is not immune to hackers and that the average bitcoin account is not completely safe from hacking or other security breaches.

- Research showed that 18 out of 40 companies that offered to exchange bitcoins into other currencies have fallen out of business and only six of them were indemnifying their customers.

- The volatility of prices is another major drawback. This means that the price of bitcoins in dollars fluctuates widely. For example, in 2013 1 bitcoin was worth about 13 USD. After that, the price quickly rose to USD 1,200 and now stands at around USD 573 (as of August 28, 2016). This again means that if you switch to bitcoin it is important that you hold onto them as switching back can lead to a significant loss.

Understand the risk of investing in bitcoin. A popular way to use bitcoins is as an investment and a particular caution is advised here before proceeding. The main risk of investing in bitcoin is the extreme volatility. The risk of big losses is life-sized with prices going up and down quickly.

Understand the risk of investing in bitcoin. A popular way to use bitcoins is as an investment and a particular caution is advised here before proceeding. The main risk of investing in bitcoin is the extreme volatility. The risk of big losses is life-sized with prices going up and down quickly. - In addition, because the value of bitcoins is determined by supply and demand, the amount of people willing to use bitcoins could be greatly reduced by government research and regulation, which could theoretically make the currency worthless.

Part 3 of 6: Set up storage for bitcoins

Store your bitcoins online. Before you can buy bitcoins, you first have to set up a storage place for your bitcoins. This is the first step in purchasing bitcoin. At the moment you can store your bitcoins online in two ways:

Store your bitcoins online. Before you can buy bitcoins, you first have to set up a storage place for your bitcoins. This is the first step in purchasing bitcoin. At the moment you can store your bitcoins online in two ways: - Store the keys to the bitcoins in an online wallet. The wallet is a computer file that holds your money just like a wallet. You can set up a wallet by installing the bitcoin client, which is a piece of software that controls the currency. However, if your computer gets hacked by a virus or hackers, or if you lose the files, you can lose your bitcoins. Always make a backup of your wallet on an external drive to avoid losing your bitcoins.

- Store your bitcoins through a third party. You can also set up a wallet with a third party such as Coinbase or blockchain.info, where your bitcoins are stored in the cloud. This is easier to set up, but you have to entrust your bitcoins to a third party. These sites are two of the larger and more reliable third parties, but there is no guarantee as to the security of these sites.

Create a paper wallet for your bitcoins. One of the most popular and cheapest ways to secure your bitcoins is a paper wallet. The wallet is small, compact and made of paper with a code. An advantage of a paper wallet is that the keys for the wallet are not stored online. So they are not prone to cyber attacks or hardware issues.

Create a paper wallet for your bitcoins. One of the most popular and cheapest ways to secure your bitcoins is a paper wallet. The wallet is small, compact and made of paper with a code. An advantage of a paper wallet is that the keys for the wallet are not stored online. So they are not prone to cyber attacks or hardware issues. - Several online sites offer services for bitcoin paper wallets. They generate a bitcoin address for you and create an image with two QR codes. One is a public address that you can use to receive bitcoins and the other is private and is used to spend bitcoins stored at the address.

- The image is printed on a long piece of paper that you can then fold in half and carry with you.

Use a physical wallet to store your bitcoins. Physical wallets are very limited and difficult to obtain. They are special devices in which private keys are stored electronically and with which payments can be facilitated. Physical wallets are usually small and compact and look like a USB stick.

Use a physical wallet to store your bitcoins. Physical wallets are very limited and difficult to obtain. They are special devices in which private keys are stored electronically and with which payments can be facilitated. Physical wallets are usually small and compact and look like a USB stick. - The Trezor physical wallet is ideal for bitcoin miners who want to purchase large amounts of bitcoins, but don't want to rely on third parties.

- The compact Ledger bitcoin wallet functions as USB storage for your bitcoins and uses smart card security. It is one of the more affordable physical wallets on the market.

Part 4 of 6: Exchanging Bitcoins

Choose a shuttle service. Buying bitcoins through exchange is the easiest way to get bitcoins. An exchange works just like exchanging other currencies: You sign up and exchange your own currency for bitcoins. There are hundreds of possible exchange services and the best one for you depends on where you are, but the best known include:

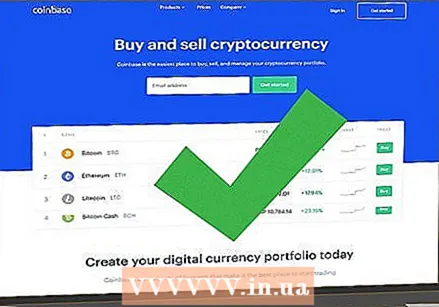

Choose a shuttle service. Buying bitcoins through exchange is the easiest way to get bitcoins. An exchange works just like exchanging other currencies: You sign up and exchange your own currency for bitcoins. There are hundreds of possible exchange services and the best one for you depends on where you are, but the best known include: - CoinBase: This popular wallet and exchange service also trades USD and EUR against bitcoins. The company uses the internet and mobile apps to facilitate buying and selling bitcoins.

- Circle: This exchange service allows users to store, send, receive and exchange bitcoins. Currently, only US residents can link their bank account to deposit funds.

- Xapo: This bitcoin debit card provider offers regular currency deposits, which are then converted to bitcoin on your account.

- With some providers you can also trade in bitcoins. Other exchange services act as wallet services with limited buying and selling options. Most exchangers and wallets store digital or regular currencies for you, just like a regular bank. Exchangers and wallets are a great option if you want to engage in regular trading and don't need anonymity.

Prove your identity and provide contact information to the service. When you sign up for an exchange service, you must provide personal information to the service to open an account. Most countries require by law that any individual or financial system using a bitcoin exchange service meet the requirements related to money laundering.

Prove your identity and provide contact information to the service. When you sign up for an exchange service, you must provide personal information to the service to open an account. Most countries require by law that any individual or financial system using a bitcoin exchange service meet the requirements related to money laundering. - Although you must be able to prove your identity, exchangers and wallets do not offer the same protection as banks. You are not protected against hackers and you will not receive any compensation if the company goes bankrupt.

Buy bitcoins with your exchange account. Once you open an account with an exchange service, you will need to link it to an existing bank account and transfer the necessary funds to and from your new bitcoin account. This is usually done by wire transfer and a fee must be paid for it.

Buy bitcoins with your exchange account. Once you open an account with an exchange service, you will need to link it to an existing bank account and transfer the necessary funds to and from your new bitcoin account. This is usually done by wire transfer and a fee must be paid for it. - Some converters allow you to personally deposit money into their bank account. This is done in person and not through an ATM.

- If you need to link a bank account to use the exchange service, usually only banks from the country where the service is located will be allowed. Some exchangers allow you to transfer money to accounts abroad, but the costs are much higher and there may be a delay if the bitcoins are converted back to the local currency.

Part 5 of 6: Using a salesperson

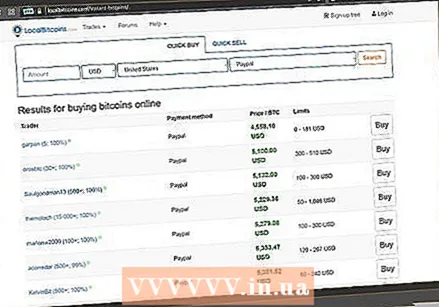

Find sellers on LocalBitcoins. This is the main site for doing personal trade with a local seller. You can set up a meeting and negotiate the price for bitcoins. The site has an extra layer of security for both parties.

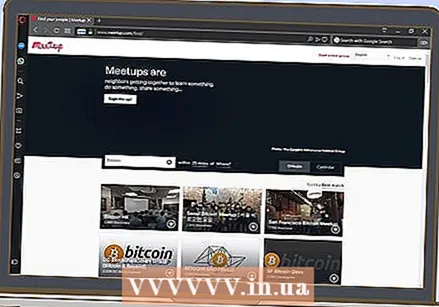

Find sellers on LocalBitcoins. This is the main site for doing personal trade with a local seller. You can set up a meeting and negotiate the price for bitcoins. The site has an extra layer of security for both parties.  Use Meetup.com to find sellers. If you're not comfortable trading one-on-one, you can use Meetup.com to trade a bitcoin meetupgroup. Anyone can then decide to buy bitcoins as a group and learn from other users, who have previously used sellers to purchase bitcoins.

Use Meetup.com to find sellers. If you're not comfortable trading one-on-one, you can use Meetup.com to trade a bitcoin meetupgroup. Anyone can then decide to buy bitcoins as a group and learn from other users, who have previously used sellers to purchase bitcoins.  Suggest the meetup fixed the price. Depending on the seller, you pay a premium of 5 to 10% on the exchange price for personal trade. You can find the current bitcoin conversion rates online at http://bitcoin.clarkmoody.com/ before agreeing to the seller 's fee.

Suggest the meetup fixed the price. Depending on the seller, you pay a premium of 5 to 10% on the exchange price for personal trade. You can find the current bitcoin conversion rates online at http://bitcoin.clarkmoody.com/ before agreeing to the seller 's fee. - You should also ask the seller if he wants to be paid in cash or via an online payment service. Some sellers allow payment via PayPal, but most prefer cash.

- a decent salesperson will always agree a price with you before meeting. Most will want to act quickly after setting the price, in case bitcoin's value changes dramatically.

Meet the seller in a busy, public place. Avoid meeting in private homes. Take the right precautions, especially if you have cash with you to pay the seller.

Meet the seller in a busy, public place. Avoid meeting in private homes. Take the right precautions, especially if you have cash with you to pay the seller.  Make sure you have access to your wallet. If you meet the seller in person, you must be able to access your bitcoin wallet via your smartphone, tablet or laptop. You also need access to the internet to confirm that the transaction was successful. Before paying the seller, always check whether the bitcoin has been transferred to your account.

Make sure you have access to your wallet. If you meet the seller in person, you must be able to access your bitcoin wallet via your smartphone, tablet or laptop. You also need access to the internet to confirm that the transaction was successful. Before paying the seller, always check whether the bitcoin has been transferred to your account.

Part 6 of 6: Using Bitcoin ATMs

Find a bitcoin payment terminal near you. Bitcoin payment terminals are relatively new, but they are increasing. You can use an online bitcoin vending map to find one near you.

Find a bitcoin payment terminal near you. Bitcoin payment terminals are relatively new, but they are increasing. You can use an online bitcoin vending map to find one near you. - You can find bitcoin vending machines these days at many institutions, from universities to local banks.

Withdraw cash from your bank account. Most bitcoin payment terminals only accept cash, because they are not designed to process credit card transactions.

Withdraw cash from your bank account. Most bitcoin payment terminals only accept cash, because they are not designed to process credit card transactions.  Put your cash in the payment terminal. Then scan the QR code of your mobile wallet or use the codes that come with your account to put bitcoins on your wallet.

Put your cash in the payment terminal. Then scan the QR code of your mobile wallet or use the codes that come with your account to put bitcoins on your wallet. - Exchange rates at bitcoin machines run from 3% to 8% on top of the regular exchange price.

Tips

- Be careful with bitcoin mining. "Mining" means that you create your own bitcoins by forming blocks of bitcoin transactions. although mining is technically a way to 'buy' bitcoins, the popularity of bitcoin has made mining bitcoins more difficult and is mainly done by specific mining groups called 'pools' or by companies dedicated to it set up. You can buy stock in a pool or a mining company, but it is no longer something that an individual can do on their own to generate a profit.

- Be careful of people who try to sell your software, which you could use to mine bitcoins on a regular computer, or bitcoin mining equipment. This is probably a scam and will not help you with mining bitcoins.

- Make sure your operating system is reasonably safe. On a Windows computer, use VirtualBox, set up a Linux virtual machine (Debian, for example), and only work with bitcoins in this virtual machine. When it comes to desktop wallets, Electrum (electrum.org) is the best right now.